Money goes into the energy system primarily through consumers paying their bills. This section therefore begins with examining how these bills are structured, and how pricing is set.

Dissecting the energy bills

The price of energy

Domestic

Most domestic electricity and gas tariffs are in two parts:

- A simple cost of energy that is a fixed price per unit of energy consumed (in pence /kWh)

- A fixed standing charge that is paid per day, regardless of what the consumer does (in pence/day or £/year).

Some people are on ‘Economy 7’ tariffs, which are a basic form of time of use tariff, with two different tariffs in use at different times (daytime/nighttime).

These vary according to the energy supplier, the specific tariff, the region, and the means of payment. These prices are shown on energy bills, but the bill can be confusing to read. Citizens Advice provides support with understanding your energy bill.

Overall average in Great Britain, 2018 figures

| Gas | Electricity | |

| Standing charge (fixed cost) | £85.25/year23.3p/day | £81.15/year22.2p/day |

| Cost of energy | 3.73 p/kWh | 15.5p/kWh |

| Overall average | 4.3p/kWh (based on 15,000kWh in a year, total bill £646) | 17.5p/kWh (based on 3800kWh in a year, total bill £668) |

Non-Domestic

The unit price paid by non-domestic customers is lower than that paid by domestic consumers. The cost of supplying and billing per unit of energy is less for consumers who use a lot of energy, due to the fixed costs per customer. This type of cost-structure incentivises consumers to use more energy – not what we want from an environmental point of view (see ‘rising block tariff’ discussion below for an alternative).

Price of gas and electricity for non-domestic consumers, 2018 figures

| Gas | Electricity | |

| Average non-domestic | 2.3 p/kWh | 11.4p/kWh |

| Smallest user category | 3.9 p/kWh(<278 MWh/year) | 15.2p/kWh(<20MWh/year) |

| Biggest user category | 1.8 p/kWh(>277,777 MWh/year) | 9.6p/kWh(>150,000 MWh) |

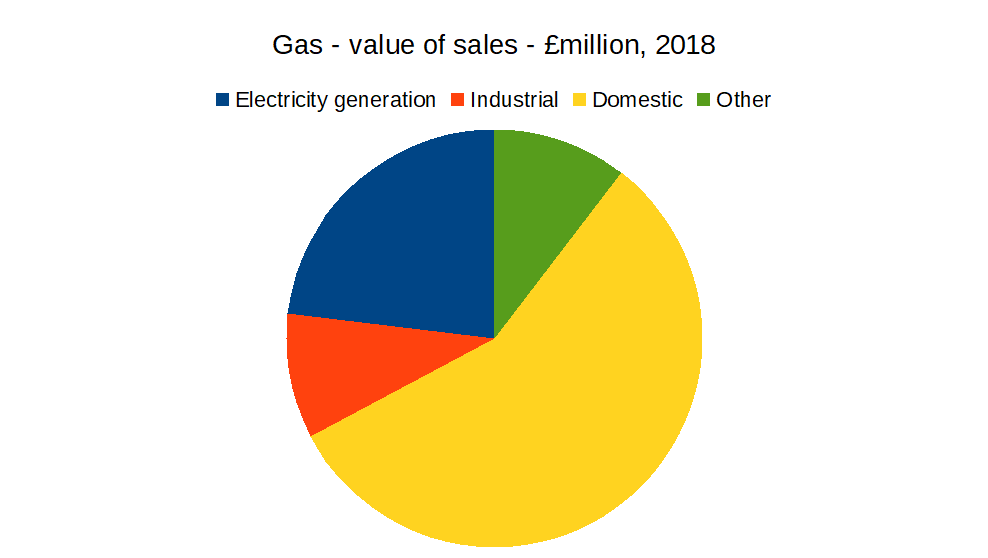

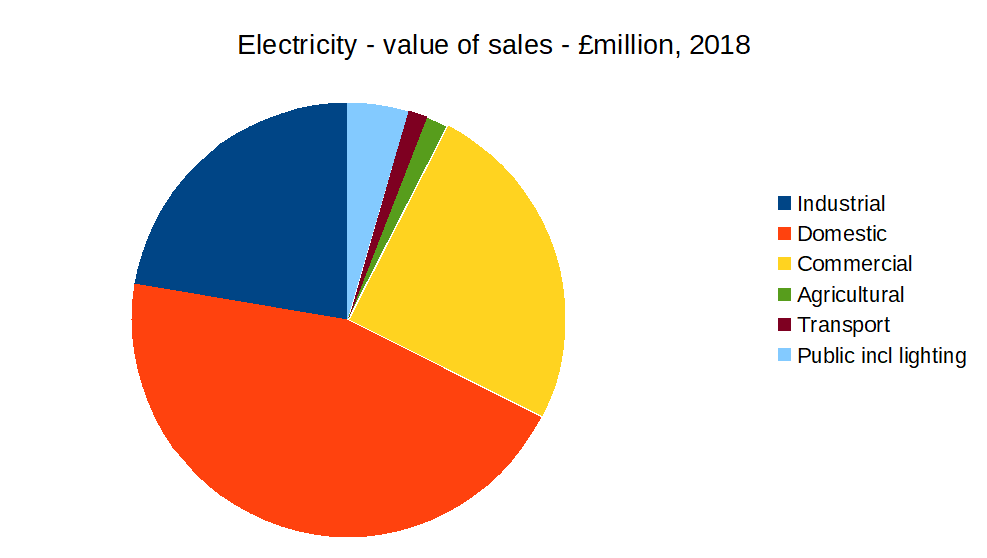

The pie charts below show where the income from sales comes from, by sector. This shows that the domestic sector provides the majority of the sales value for gas (56%), and the biggest portion of the sales value for electricity (45%) (based on figures from Digest of UK Energy Statistics, DUKES 2019 chart 1.7):

Politicians like to promise lower bills by focusing on the price of energy. However, making energy affordable is more complex than that. Just reducing prices can have the undesirable side-effect of making investment in energy efficiency less cost-effective. Other approaches include:

- Changing the structure of tariffs

- Reduce the amount of energy needed for a given level of service (e.g. insulate homes)

- Deeper lifestyle changes such as travelling less or changing how we use buildings.

Tariff structures

There are alternative approaches to structuring tariffs. Some of these make the tariffs more cost-reflective, others less, but better at providing access to energy and incentives for pro-environmental and pro-social consumption behaviour. The Centre for Sustainable Energy published a report for the National Consumer Council in 2008 reviewing a number of sustainable energy tariff options. Although it is more than 10 years old, the thinking and analysis involved is still relevant.

Most of the tariff structures described below require more advanced metering. Customers who are already on Economy 7 meters have two meters which are active at different times of day. Larger non-domestic consumers have half-hourly meters, which record how much electricity was used in each half hour. The roll out of smart meters will enable more complex metering information to be recorded. Some domestic tariffs e.g. Octopus agile tariff now offer half hourly tariffs to domestic customers.

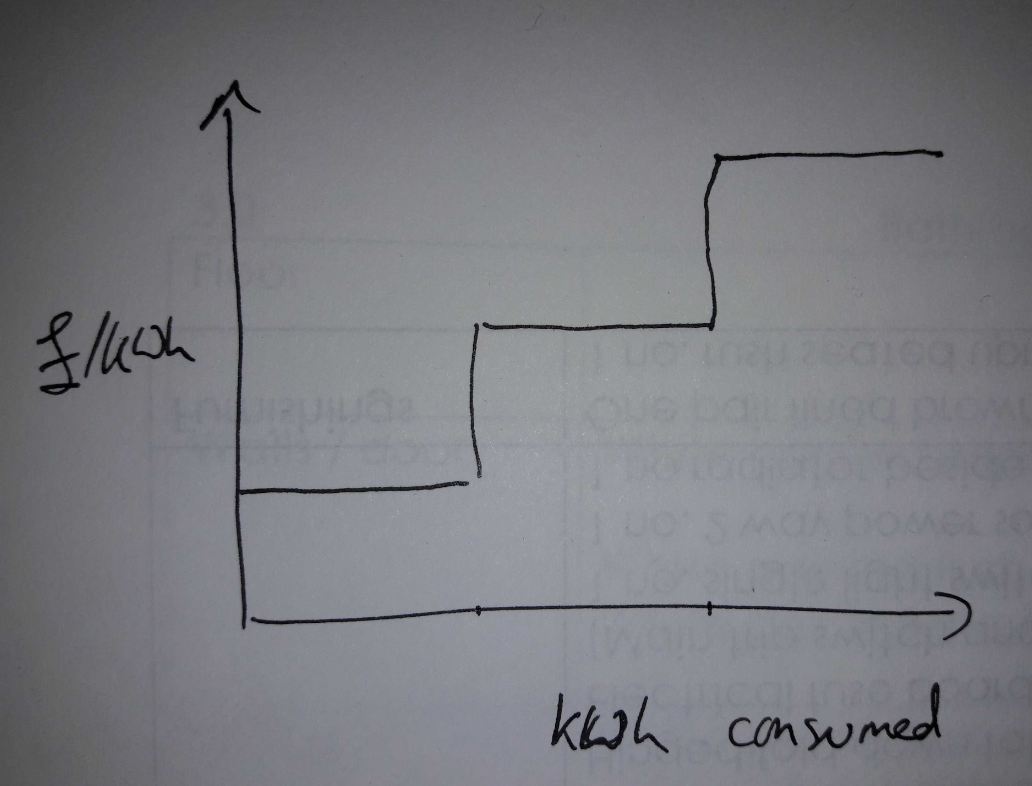

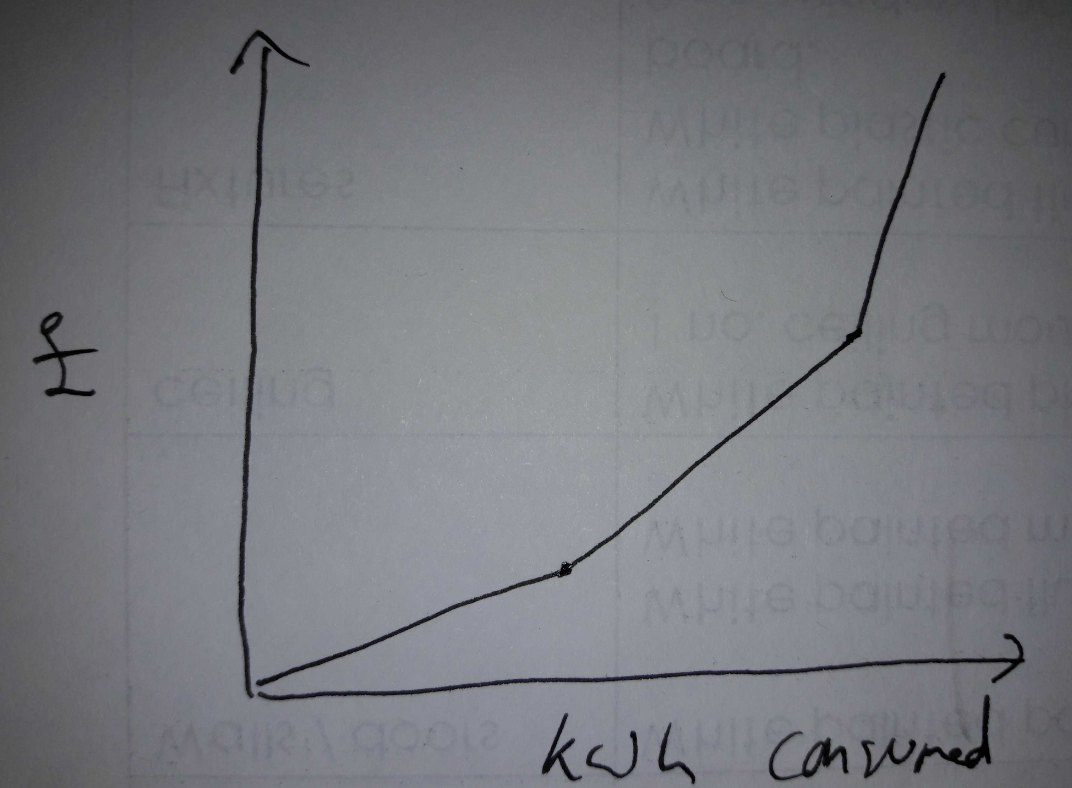

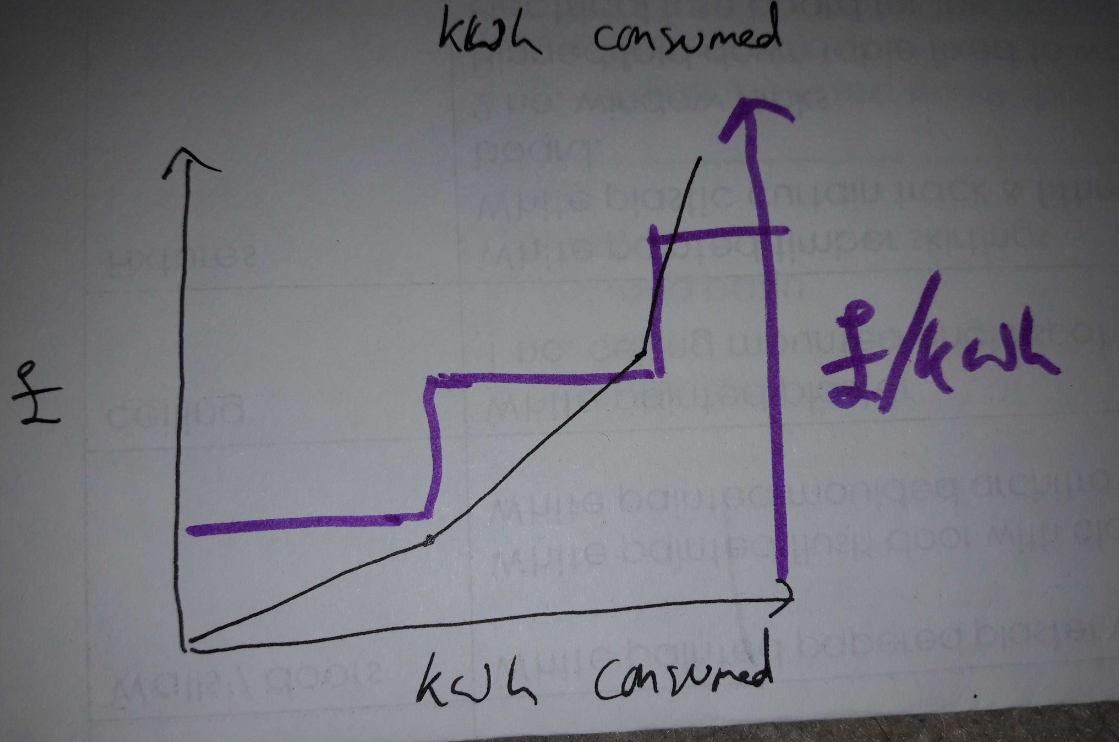

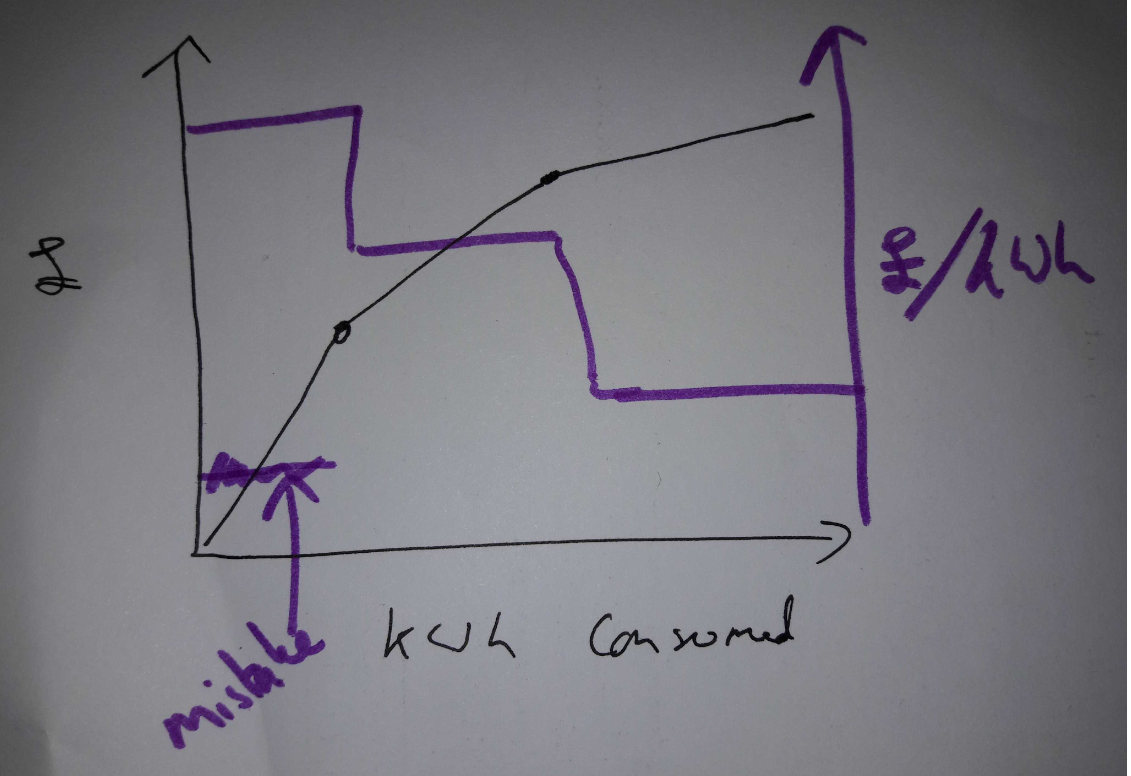

Rising block tariff

How can we ensure that everyone has access to a basic amount of energy, and that energy efficiency pays, and lower consumption is rewarded? One approach is to use a ‘rising block tariff’. This means that the price of electricity is structured in blocks according to the amount consumed, and that the price rises with each block. A consumer using a small amount of electricity pays less per unit than a consumer using a large amount.

This is in contrast to the current system, where the more energy you use the less you pay per unit:

In order for this pricing to pay for the energy system overall, there has to be cross-subsidy from larger to smaller consumers – i.e. households or businesses who use a lot of energy pay more than the cost of providing that energy to them. This does not conform with ‘cost reflectiveness’, but this tariff structure is commonly used in many countries.

According to Wikipedia, some form of rising block tariff is used in countries including: Bahrain; Brunei; Quebec; Egypt; Indonesia; Iraq; South Korea; Laos; Malaysia; Pakistan; Paraguay; Sri Lanka; Taiwan; Thailand; Tunisia; Uganda; Zambia. Many of these are based on daily or monthly consumption blocks.

The idea of a rising block tariff is not so alien to British politics. In October 2008 an early day motion was tabled by 41 MPs to consider a rising block tariff as part of statutory reforms to the GB energy system. You can see who supported it on the parliament website. They argued that a rising block tariff “has the merits of encouraging careful management of energy used by householders, promoting an element of re-distribution, reducing the need for means-testing for social tariffs and reducing carbon dioxide emissions”.

There are some social justice risks that would need to be considered . In particular, households who for some reason have unusually high energy service needs, e.g. for medical reasons, could suffer from paying in the high-consumption bracket.

Given that a rising block tariff requires cross-subsidy between different parts of the system, it cannot be implemented unilaterally by e.g. a municipally owned or community owned energy company within a competitive system. Some kind of legislative change at national level is essential.

Tariffs to manage peak demands

As discussed in the section on flexibility, time balance is increasingly important and challenging for the electricity system. The electricity system as a whole would be cheaper and have less environmental impact if peak consumption levels reduced. Currently, most domestic consumers have no financial incentive to use electricity at off-peak times.

There are a number of ways of doing this. Broadly they can be categorised as:

There are a number of ways of doing this. Broadly they can be categorised as:

- Demand-response payments

- Payments for turning down demand (or turning up generation on the ‘demand side’ of the meter) in response to a request from a contracting party

- Time of use tariffs – charging more when electricity is more expensive

- Fixed time of use tariffs with published peak and off-peak times (economy 7 is an example of this)

- Variable time of use tariffs – where the price of electricity at a given time of day varies from day to day depending on wholesale market prices.

- Limiting peak consumption

- In absolute ways – e.g. ‘you may not use more than 5kW at one moment’

- Charging for the peak consumption level – also called ‘demand charging’

From a cost-reflectiveness perspective, the electricity provided at peak times is much more expensive for the supply company to buy on the wholesale market than electricity provided at off-peak times, and this difference is likely to increase. Full cost reflectiveness would mean that the cost of peak-time electricity would be passed on to the consumer.

Demand response

One approach to achieving flexibility in electricity consumption is through payments for demand response. These payments currently exist for very large scale responses, paid for by National Grid, and some DNOs are starting to develop local demand response markets.

This is the income that commercial aggregators, introduced in the organisations and ownership chapter use. It is the main business model considered by the Carbon Coop/Regen/CES ‘Energy Community Aggregator Service’ model. Demand response payments are sometimes structured into two parts:

- [format bullet points as blue text colour]

- An availability payment, which is paid whether the demand response service is used or not

- A utilisation payment, which is paid for the amount of energy demand that has been switched off for a specific time period when instructed.

This approach is difficult to apply to domestic consumers, because it requires automated control of energy asses in the home, and the cost of recruitment, contracting and metering are high. It is also difficult to prove whether someone would have been using electricity at any particular moment – how do I demonstrate that I abstained from charging my electric car during a demand response hour, rather than just happened not to use it?

Time of use tariffs

An alternative to active demand response which may work better for domestic consumers is a time of use tariff. Rather than being paid for avoiding consumption that would otherwise have happened, electricity is simply more expensive at some times than others, creating a financial incentive for the user. These can be:

- Fixed time of use tariffs with published peak and off-peak times (economy 7 is an example of this)

- Variable time of use tariffs – where the price of electricity at a given time of day varies from day to day depending on wholesale market prices.

There are distributional equality risks with time of use tariffs – as they risk penalising people who have to use energy at particular times – e.g. households with children, people with non-flexible working patterns – and making things harder for people on low incomes who may also have less ability to shift around their energy consumption. Variable time of use tariffs in particular could require people to plan ahead and keep monitoring forecasts of electricity prices in order to respond.

Many responses can be automated. This could include ‘smart’ white goods – fridges, freezers, washing machines which can be automatically controlled to respond to different energy prices. However, it is likely that the bulk of effective time of use response would be achieved by bigger and less time-sensitive loads, e.g.

- Electric vehicle charging

- Electric heating, including using immersion heaters to heat water when electricity is cheap, and heat pumps to heat buildings

- Air cooling

- PV and batteries

Limits to peak consumption

The island of Eigg, in north west Scotland, has its own independent electricity system owned by the community. They have a 5kW limit for domestic consumers, and 10kW for businesses. If a household goes over 5kW, their electricity automatically cuts off, and they have to go to the maintenance team to get re-connected. 5kW is the approximate equivalent of two normal-power kettles or toasters.

Other places, e.g. Italy have tariffs which are structured a bit like the Eigg system – if you have a 5kW tariff, your supply gets cut off if you go above 5kW.

Demand charging

Demand charging shifts the focus of energy prices from the amount of energy used, to the peak power used, by a price on the capacity of your supply (remember the discussion of energy and power in the physics of energy chapter?). This is a bit similar to having a limit on demand – just with a different charging structure, rather than a legal limit.

That means a charge for having everything on at once, rather than for having something on all day.

It could be a component of a tariff, alongside an energy charge – the way that the standard tariff has a standing charge as well as an energy price. It could be seen as a more nuanced approach to a standing charge. This shift in focus from variable to fixed costs mirrors the shift in cost structure from a cost of energy (MWh) in a fuel-consuming system, to a cost of infrastructure (MW) in a renewable energy system. [link to relevant comment in ‘cost structure’ section.

Hybrid approach

It could be possible to have a rising block tariff for energy, combined with demand charging. What if we had a rising block component of a bill, for example:

- 0-20kWh/day – 10p/kWh

- 20-30kWh/day – 20p/kWh

- 30-50kWh/day – £1/kWh

And a standing component of the bill that depends on peak consumption, for example:

- 0-3kW – 5p/day

- 3-5kW – 10p/day

- 5-10kW – 50p/day

- >10kW – £1/day

What if allowances were made for people with high energy needs for medical reasons?

A big challenge in devising such a tariff structure would be to make it cover overall energy system costs reliably over time, as cross subsidy to incentivise pro-social behaviour is vulnerable to not adding up if people change their behaviour differently to what was predicted. Some kind of overall responsiveness to information about consumption patterns may be needed – i.e. good and quick informational feedbacks. For example, if the lowest cost brackets were set at below cost price to encourage people to be energy efficient, and most people became highly energy conscious and consumed within the 0-20 kWh/day and 0-3kW bracket, the price of energy at that level of consumption may need to go up in order to cover the system costs overall.

Perhaps some clever system involving average consumption levels could be designed. Maybe something like this:

- Lowest consumption quartile – 10p/kWh

- Second and third consumption quartile – 20p/kWh

- Highest consumption quartile – £1/kWh

- Lowest peak quartile – 5p/day

- Second and third peak quartile – 10p/day

- Between third quartile and highest decile – 50p/day

- Highest peak decile – £1/day

Heat Networks

Heat networks are not regulated, and operate at a local scale. There isn’t the same national competitive market for heat through regulated energy suppliers as there is for electricity and gas. Customers buying their heat from a district heating network are usually purchasing from a natural monopoly. This means that the usual form of consumer protection that Ofgem works towards, of choice in a competitive market, is not available.

Heat network customers are entitled to opt out of the heat network and use electric heating instead, or to have their home connected to the gas network. However, it is likely that they would have to pay an exit fee or have some other cost to exiting the heat network contract, and if their home is not connected to the gas network they may have to pay to be connected, which is likely to be prohibitive.

From the perspective of the heat network operator, having enough customers to buy heat over the long term is essential to viability. The possibility that a critical mass of customers may opt out of the network is a risk for investment in heat networks, and can prevent an otherwise viable project from going ahead or make the cost of capital much higher.

One way of addressing some of these challenges can be to develop co-operative based heat networks, where the consumers are co-owners of the network, and have full transparency and control over the management and finances. For example, a co-op would allow consumers to select contractors to carry out operation and maintenance, and to make decisions on prices etc. This is described in more detail under ‘new business models.

Other sources of income

Significant investment is needed to transition the energy system to zero carbon, and the cost of capital (discussed under cost structure) is much lower when income is secure. There is a case to be made for policy-based additional income to the energy system, through various forms of subsidy. In economics language, this is primarily because of the positive externalities (benefits that go to everyone rather than to the investor/owner) of addressing climate change, or conversely the negative externalities of burning fossil fuels.

There are various policies in place to incentivise long term investment in the energy system and achieve energy security. This includes support for renewable energy and the electricity market reform act 2013.

This is where energy democracy is so crucial. If we don’t take democratic power, energy industry lobbyists shape policies in favour of incumbent systems, or technologies with high potential profits. The detail is tedious, but it is essential to make it more transparent.

Tax (and tax breaks)

One component of the energy bill is tax. Domestic gas and electricity are taxed with a low rate of VAT, at 5%, rather than the normal 20%. Tax on petrol and diesel has also been frozen since 2011. This is a tax break for energy, and since most of this energy is currently from fossil fuels, it amounts to a tax break on fossil fuels.

In 2016, the UK was the bigest provider of subsidy to fossil fuels in the EU, mainly in the form of tax breaks. The north sea oil industry receives taxpayer funds, particularly to cover the cost of decomissioning old oil and gas fields, and cost the UK taxpayer a net total of £396m in 2016.

Support for renewable energy

Support for renewable and low carbon energy has been in place in various forms for many years. The structure of this support has been changing, and has overall reduced in recent years. This reduction in support has been partially offset by the redution in cost of renewable energy generation. However, this does not level the playing field with fossil fuels, due to the incumbent advantage they have, and tax breaks they receive.

There is also now support for energy system services providing flexibility. Flexibility is needed to support for the role of renewable energy within the system, but in practice most of the flexibility itself has itself come from diesel and gas generators, particularly at distribution level. This is part of the electricity market, and changes have been implemented through the 2013 Electricity Market Reform Act.

Historic approaches:

- ROC – Renewable Obligation Certificate – From 2002, all electricity suppliers in GB had a requirement to source a percentage of their electricity from renewable sources. If they did not generate this themselves, they could meet the requirement by buying ‘renewable obligation certificates’, which were issued to all generators of renewable energy (this allows greenwashing of energy tariffs). From March 2017 new schemes were no longer able to get ROCs, but existing schemes continue to receive them.

- Feed in Tariff (FiT) – from 2009, the Feed in Tariff was available to small-scale renewable electricity generators. This is a fixed payment per unit of electricity generated, whether that electricity is used on site or not, accompanied by an ‘export tariff’ for electricity exported. In many cases, the amount exported is not actually measured, and so is ‘deemed’. Both tariffs are paid over a fixed time period of 20-25 years, depending on the technology. The FiT stopped accepting new applications in March 2019.

- Renewable Heat Incentive (RHI) – this was the first ever incentive for generating renewable heat, including support for heat pumps, solar thermal, biogas, and biomass. Creating a renewable heat incentive was a bold move, and is a complex thing to administrate. It hasn’t done enough to decarbonise heat, and the climate impact of switching to biomass depends on the source of biomass, which isn’t sufficiently taken into account. The RHI scheme in Northern Ireland was mis-adminstered and failed.

Electricity Market Reform:

In 2013 the Electricity Market Reform Act was passed, and brought in contracts for difference and the capacity market.

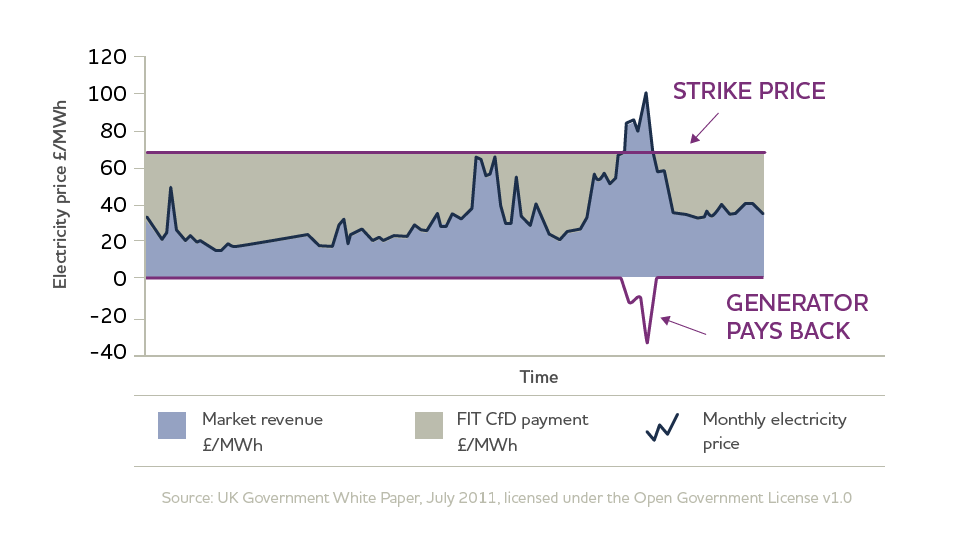

Contracts for Difference

This was a new approach that replaced the ROC from October 2014, and works like a reverse auction. It allows low carbon energy generators to make a long term contract to receive a fixed price for their electricity, called the ‘strike price’. This is made up of a combination of revenue from the market price, the revenue, and a payment for ‘the difference’, from a government owned company called the Low Carbon Contracts Company (LCCC).

The strike price is set through an auction process. There are two separate auction pots – one for ‘established technologies’ and one for ‘less established technologies’, which are separated in order to give less established technologies the opportunity to get a higher price. The 2019 Auction Results are available here.

Less established technologies

- Advanced Conversion Technologies

- Anaerobic Digestion (> 5MW)

- Dedicated Biomass with CHP

- Geothermal

- Offshore Wind

- Remote Island Wind (> 5MW)

- Tidal Stream

- Wave

More established technologies

- Onshore wind (>5MW),

- Solar Photovoltaic (PV) (>5MW),

- Energy from Waste with CHP,

- Hydro (>5MW and <50MW),

- Landfill Gas and Sewage Gas

The University of Exeter’s iGov project criticises the way the CfD was set up for favouring nuclear power over renewable energy. This is partly because nuclear power is a baseload – which generates steadily all the time – and baseload generators have a reference price set based on the average annual wholesale price. On the other hand, variable generators (i.e. renewable energy) have the reference price set based on the day ahead market. This means when wholesale prices are high, nuclear power can make a lot of money, but renewable energy can’t. Additionally, there is a limit on total spend, and if expensive nuclear power soaks a lot of this up, there won’t be much left for renewable energy.

The nuclear power industry probably had a lot more of a say in the design of the CfD system than you or I did.

Capacity Market

The Electricity Market Reform of 2013 also included the introduction of a capacity market. This is supposed to make sure that dispatchable generation or storage based supply to fill gaps when renewable energy is not generating – a large-scale approach to providing flexibility. Currently the most efficient form of large scale, fossil fuel based dispatchable generation is the Combined Cycle Gas Turbine, or CCGT.

The concern behind the capacity market is that as more of the energy generated is from renewable sources, the ‘utilisation rate’ of conventional responsive generators such as CCGTs will go down (they would generate for fewer hours each year). This means that their income from selling energy will go down, and so there may not be enough investment in new CCGTs to fill the gaps when renewable energy is not generating. Having a way to ensure there is enough ‘capacity’ to generate peak power, in MW, is important for reliability of the electricity system. In the Capacity Market providers are paid monthly to be available to provide additional electricity on demand from the system operator. The monthly price is set at an auction.

Many technologies can play this role in addition to CCGTs. Options that are better for getting to zero carbon include electricity storage such as batteries, ‘Demand Side Response’ (DSR) of reducing consumption when required, interconnection of the GB electricity system with other countries, and permanent demand reduction can also be used, and should be part of the future. Options that are worse include diesel generators and open cycle gas turbines can also provide capacity at a small scale.

Catherine Mitchell from iGov describes how the capacity market will work:

“The Implementing document sets out how GB’s CM will work and how it will be paid for. Capacity will be paid for by its availability – whether or not it is used. There is also a payment for the energy component of that capacity via the market when a capacity event is triggered. The price paid for the capacity will be the marginal bid (i.e. all those which bid in below the final marginal bid will receive the higher marginal bid) via a decreasing clock auction. There are two interlinked auctions: one, to be held 4 years ahead of delivery (the first take places in December 2014 for capacity in 2018-9, for a period of up to 15 years depending on the contract agreed); and then a demand auction, a year ahead of delivery (ie for demand response to be available a year later, for a year).”

The Capacity Market has been criticised by iGov for:

- Making it difficult for demand side response to access the payments

- Not actually supporting new CCGTs

- Extending the lifetime of high carbon coal

- Supporting new inefficient diesel generators and open cycle gas turbines

There are other approaches that could be taken. For more iGov commentary on this policy, see their ‘Capacity Market Primer’.